The popular 50/30/20 rule suggests:

50% for necessities (rent, food, utilities)

30% for wants (entertainment, shopping, travel)

20% for savings & investments

But real life is not always that simple!

If your income is low, necessary expenses may exceed 50% of it.

If your income is high, your spending may rise proportionally, making the 30% discretionary limit unrealistic.

So, what’s the solution? Create your own personalized budget rule!

Follow these 8 practical steps to take charge of your finances:

1. Track Your Daily Expenses Using Smart Apps

Tracking expenses is the foundation of effective budgeting. If you don’t know where your money is going, it’s nearly impossible to manage it well. Fortunately, technology has made this process easier with apps like Jupiter, which help you automatically track expenses and categorise them.

These apps sync with your bank accounts, credit cards, and digital wallets, providing real-time insights into your spending habits. Alternatively, you can maintain a manual record in an Excel sheet or a notebook, but it is time-consuming. The best budget-tracking apps can reduce manual work and save time. This helps in developing financial awareness and being able to identify unnecessary spending. This step is crucial in understanding your cash flows and making informed decisions about where to cut back and where to invest more. This helps you spot unnecessary spending patterns.

2. Categorize Expenses Into Essentials & Non-Essentials

Once you start tracking your expenses, the next step is to categorize them into essentials (needs) and non-essentials (wants). Essentials include necessary expenses such as rent, groceries, utility bills, insurance, healthcare, transportation, and loan repayments. These are the costs you cannot avoid. Non-essentials, on the other hand, include discretionary expenses like dining out, shopping, vacations, entertainment subscriptions, and hobbies.

Additionally, there are irregular or periodic expenses, such as annual insurance premiums, home maintenance, or car servicing, which require planning but don’t occur monthly.

Categorising expenses helps you prioritise spending and identify areas where you can cut back without compromising on your basic needs.

3. Set Limits for Non-Essential Expenses

After categorising expenses, it’s important to set spending limits, especially for non-essential purchases. By defining a cap for discretionary expenses, such as ₹5,000 per month for entertainment and shopping, you create a system that prevents overspending.

Many budgeting apps allow you to set these limits and provide real-time alerts when you exceed them. This ensures that your lifestyle expenses do not get out of hand while still allowing room for leisure and enjoyment. The goal is not to completely eliminate fun spending but to keep it in check so that it does not interfere with your savings and financial goals. There might be emergency cases where we need to spend enough, but to make sure we don’t get affected, we must follow the above steps.

To know more and be prepared for such emergencies, read our post on EMERGENCY FUNDS

4. Expenses May Not Reduce Instantly, But They Will Over Time

Budgeting and expense management are long-term habits, not quick fixes. When you start tracking and setting limits like cutting back on expenses, you may not see an immediate reduction in spending. However, as you become more mindful of where your money is going, you will gradually adjust your lifestyle to fit within your financial boundaries.

Instead of feeling pressured to cut expenses overnight, allow yourself time to transition into better financial habits. For example, if you are used to dining out four times a week, you may initially reduce it to three times, then twice, until it becomes a natural shift. Over time, these small adjustments lead to significant financial benefits without making you feel deprived.

5. Review Income & Expenses Monthly

A monthly financial review is a crucial step in maintaining control over your money. Set aside time at the beginning or end of each month to analyse your income and expenses. Compare budgeted vs. actual spending, identify areas where you overspent, and evaluate whether you need to adjust your spending patterns.

Here, you don’t have to sit with pen and paper; budget-tracking apps can show you the entire story of your income and expenses in a month and save you time. Just spend time while you travel or whenever you have free time in a day.

Regularly reviewing your finances also helps you recognise trends in your income and expenses, allowing you to plan for upcoming costs and savings goals. If you find that a particular expense category consistently exceeds its limit, you can make an informed decision to either cut back or adjust your budget accordingly. A monthly review ensures that you stay on track with your financial goals while adapting to any changes in income or expenses. The 50/30/20 rule is not the only solution.

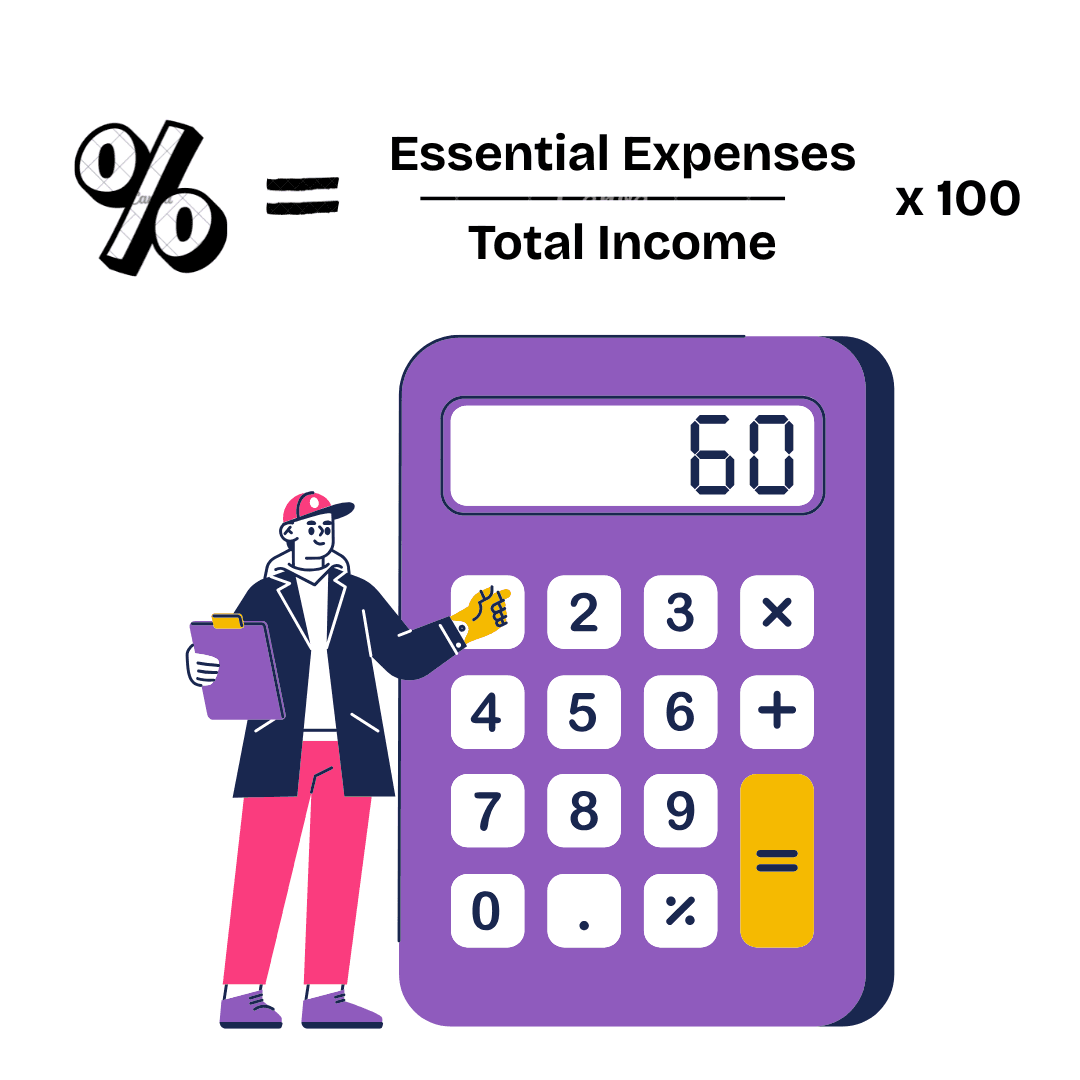

6. Calculate Essential Expenses as a Percentage of Income

To create a budget that works for you, calculate how much of your income is being spent on essential expenses. After you follow the above 5 steps, this will be a cakewalk for you. This percentage helps determine whether you are living within your means or overspending on necessities. To calculate, divide your total essential expenses by your monthly income and multiply by 100.

For instance, if your income is ₹50,000 and your necessary expenses amount to ₹35,000, your essential expenses percentage is (₹35,000 / ₹50,000) × 100 = 70%. If this percentage is too high, you may need to look for ways to reduce costs, such as finding a more affordable home, switching to a lower-cost internet plan, or reducing transportation expenses.

7. Calculate Non-Essential Expenses as a Percentage of Income

Similarly, determine how much of your income is allocated to non-essential expenses. This step provides clarity on how much you are spending on leisure, entertainment, and other discretionary activities. For example, if your discretionary expenses amount to ₹10,000 per month and your income is ₹50,000, then your non-essential expense percentage is (₹10,000 / ₹50,000) × 100 = 20%.

If this percentage is too high and prevents you from saving adequately, consider cutting back on unnecessary spending. Small changes, such as reducing impulse purchases, cancelling unused subscriptions, or opting for budget-friendly entertainment options, can help bring this percentage down.

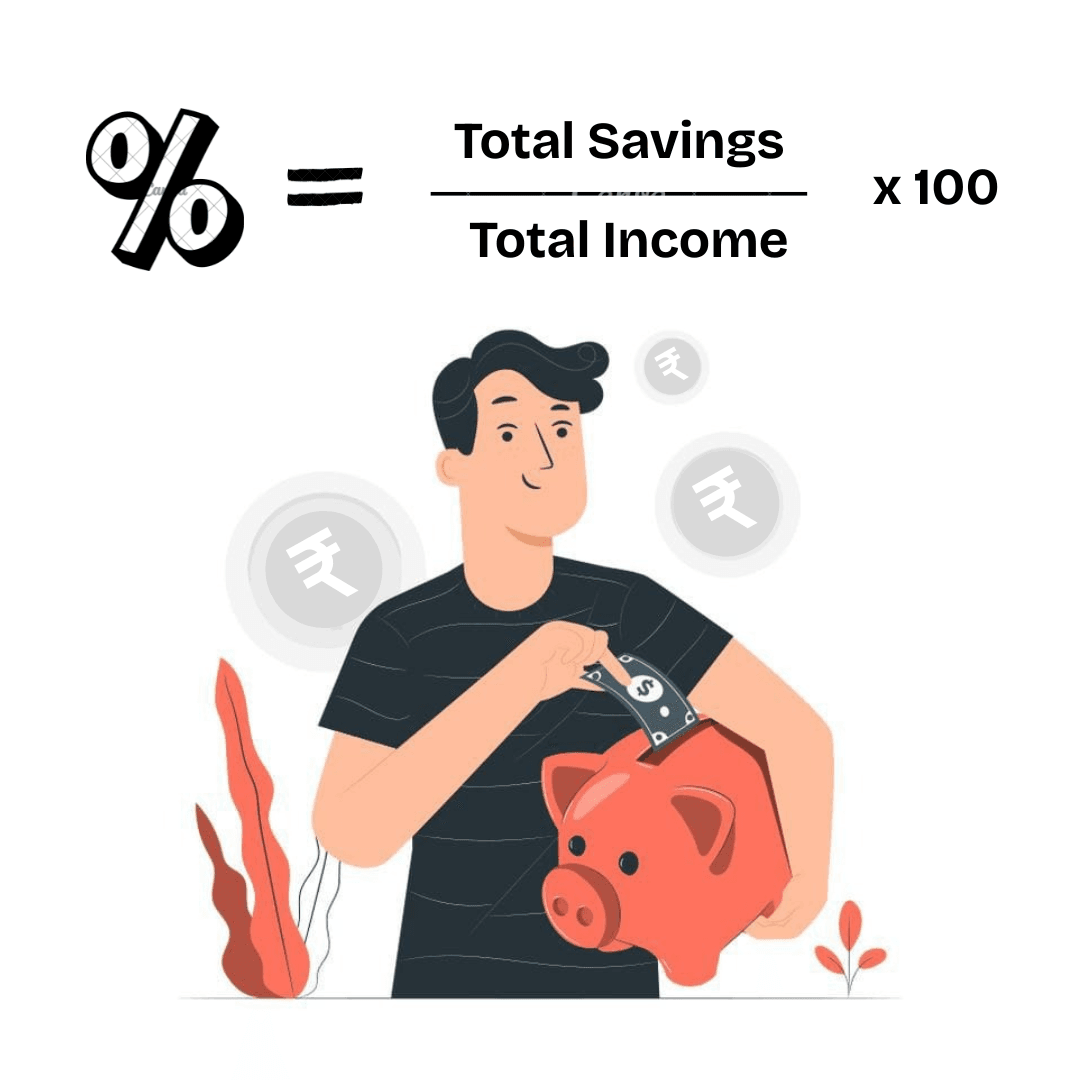

8. Calculate Savings Percentage & Adjust Your Budgeting Rule

The final step in personalizing your budget is calculating your savings percentage and making adjustments accordingly. If, after covering both essential and non-essential expenses, you find that your savings are less than 10-20% of your income, you may need to restructure your spending. For example, if your savings amount to ₹5,000 per month and your income is ₹50,000, your savings percentage is (₹5,000 / ₹50,000) × 100 = 10%.

Based on these calculations, you can create a customized budgeting rule that suits your lifestyle, such as 70/20/10 (if necessary expenses are high), 40/30/30 (if you can allocate more to savings), or 60/25/15 (for a balanced approach) instead of the 50/30/20 rule. Since expenses and income fluctuate over time, it’s important to revisit and revise your budgeting rule after a year to ensure it aligns with your current financial situation. Remember, do not revise your budget rule every few months, once you decide on your own rule, stick to it at least a year to make more informed decisions.

The idea is flexibility—your budget should adapt to your income level and lifestyle.

Conclusion: Your Budget, Your Rules!

The key takeaway is that budgeting should be flexible and personalised to your needs. Instead of forcing yourself into the conventional 50/30/20 rule, focus on tracking, categorising, reviewing, and adjusting your spending according to your financial reality. By following these eight steps, you can create a budget that works for you—whether it’s 70/20/10, 60/25/15, or 40/30/30. As your income grows, continuously re-evaluate your spending and saving strategies to maintain financial stability. Smart financial planning isn’t about restriction—it’s about control and balance. Start today and take the first step toward financial freedom!