Just like SIPs, SWPs and STPs are excellent tools to maximize the potential of your investments. Let’s explore when to use these options to accelerate your journey toward financial freedom. In this guide, we’ll explore the various types of investments in Mutual funds and help you make an informed decision.

An Overview of Introduction to Mutual Funds Investments

Mutual funds collect money from numerous investors to invest in a diversified mix of stocks, bonds, or other securities. Managed by professional fund managers, these funds aim to generate returns based on specific investment objectives, such as growth, income, or capital preservation. Whether you’re a beginner or an experienced investor, mutual funds offer a convenient way to diversify your investments, reduce risk, and achieve financial goals without the need for extensive market knowledge.

Types of Mutual Funds Investments

Mutual funds can be categorized based on various factors such as asset class, investment objective, structure, and risk profile. Here’s a breakdown of the different types of Mutual funds.

- Equity Mutual Funds:

- Invest primarily in stocks.

- High risk but high return potential.

- Suitable for long-term wealth creation.

- Types: Large-Cap, Mid-Cap, Small-Cap, Sectoral, Thematic Funds.

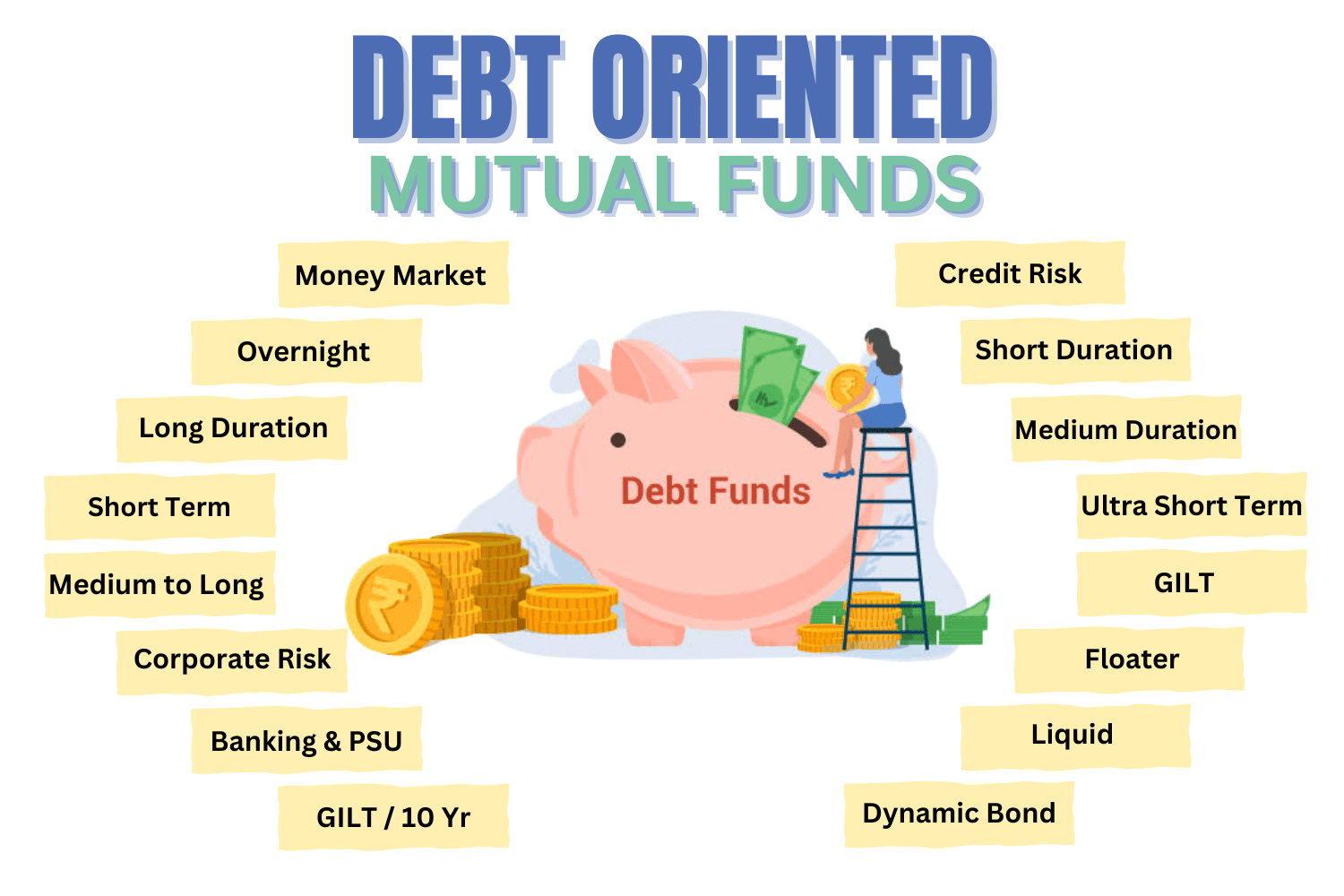

- Debt Mutual Funds:

- Invest in fixed-income securities like bonds and debentures.

- Lower risk with stable returns.

- Ideal for conservative investors.

- Types: Liquid Funds, Short-Term Funds, Gilt Funds, Corporate Bond Funds.

- Hybrid Mutual Funds:

- A mix of equity and debt investments.

- Balanced risk and return.

- Suitable for moderate risk-takers.

- Types: Balanced Advantage, Aggressive Hybrid, Conservative Hybrid Funds.

Visit these posts to learn more about all mutual fund schemes – Debt-Oriented Mutual Funds, Equity-Oriented Mutual Funds and Solution-Oriented Mutual Funds.

Benefits of investing in Mutual funds

Investing in mutual funds offers several advantages that make them an attractive choice for both beginners and experienced investors. Here are the key benefits:

- Diversification: Spreads investments across various assets, reducing risk.

- Professional Management: Managed by expert fund managers, saving time and effort.

- Accessibility and Affordability: Start investing with small amounts through SIPs.

- Liquidity: Easy buying and selling at current NAV for quick access to funds.

- Tax Efficiency: ELSS offers tax benefits, and equity funds have favourable tax rates.

- Convenience and Transparency: Easy to invest online with transparent disclosures.

- Potential for High Returns: Equity funds offer high growth potential over the long term.

- Flexibility and Variety: Multiple types of funds to suit different goals and risk levels.

- Systematic Investment and Withdrawal: Disciplined investing and organized withdrawals.

- No Lock-In Period: Most funds are flexible, except ELSS with a 3-year lock-in.

Here is a detailed circular on Mutual Funds by the Securities Exchange Board of India (SEBI) – Master Circular on Mutual Funds

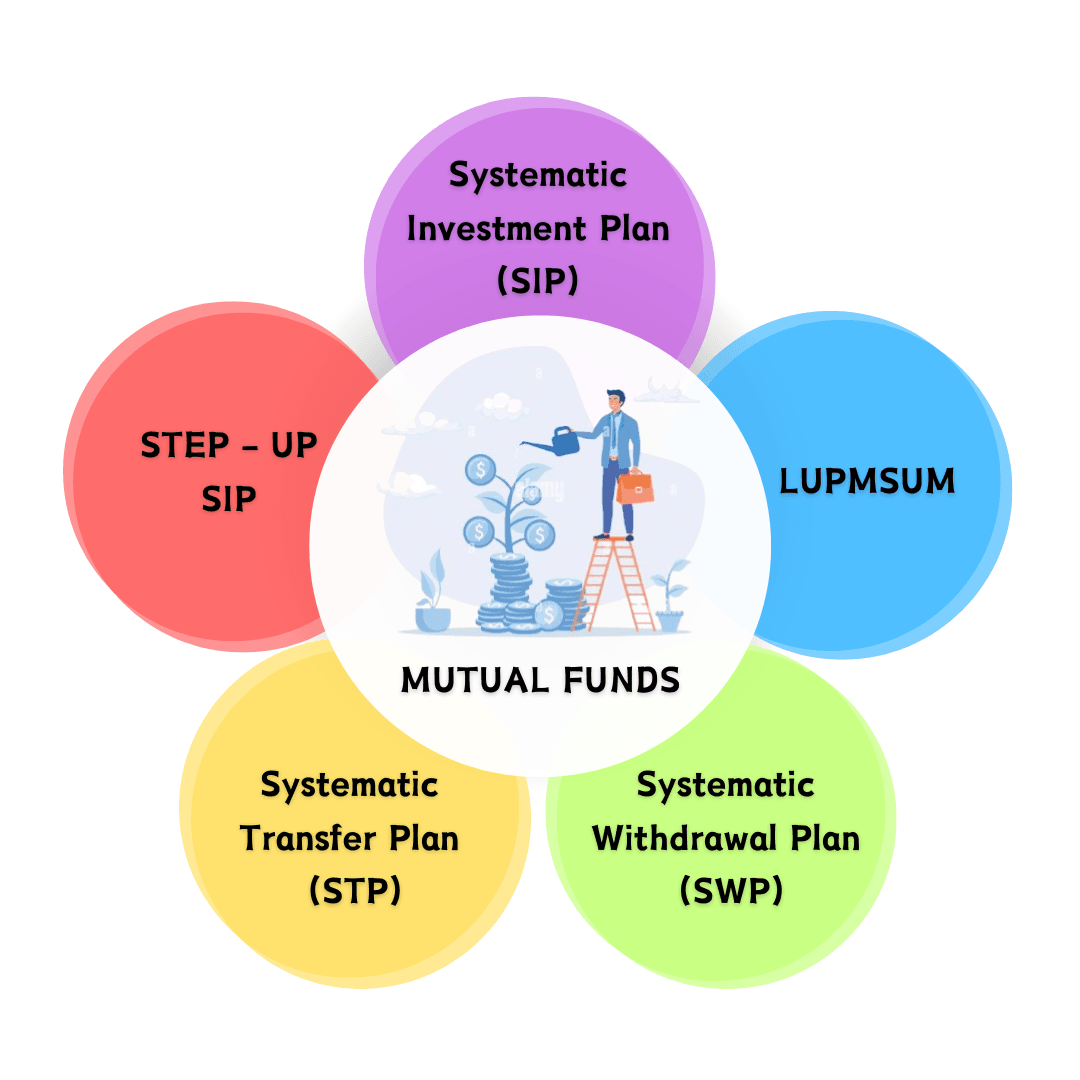

Mutual funds offer flexible investment methods to suit different financial goals and risks. From one-time investments to systematic plans, understanding these methods can help you maximize returns and manage risks effectively. Let us know different methods to invest in mutual funds.

1. Systematic Investment Plan (SIP)

A Systematic Investment Plan (SIP) is a method of investing in mutual funds where you contribute a fixed amount at regular intervals, typically monthly or quarterly. Instead of investing a lump sum, SIP allows you to invest small amounts consistently, making it easier to grow wealth over time through disciplined savings.

Let’s say for example you have been doing SIP for last 20 years and have made a good money, since you are at the age of retirement or want to get free from you

How it Works:

- A fixed amount is auto-debited from your bank account at a predetermined date.

- Units of the mutual fund are purchased based on the prevailing Net Asset Value (NAV).

- More units are bought when NAV is low, and fewer units are bought when NAV is high, benefiting from Rupee Cost Averaging.

Features of Systematic Investment Plan

- Regular Investment: Invest a fixed amount periodically, promoting disciplined savings.

- Flexibility: You can start with small amounts (as low as ₹500 per month).

- Rupee Cost Averaging: Invest at different market levels, reducing the impact of market volatility.

- Compounding Effect: Earnings on investments are reinvested, leading to compounded growth.

- No Need to Time the Market: SIPs eliminate the need to predict market highs and lows.

- Automatic Transaction: The auto-debit feature ensures timely investments.

- Goal-Based Planning: Suitable for long-term goals like retirement, education, or wealth creation.

Pros of SIP

- Disciplined Investment: Encourages regular saving and investing habits.

- Rupee Cost Averaging: Buys more units when prices are low and fewer when prices are high, averaging out cost.

- Compounding Benefits: Reinvestment of earnings accelerates wealth creation.

- Convenience: Automated payments eliminate the need for manual transactions.

- Affordability: Start investing with small amounts, making it accessible for beginners.

- Reduces Market Timing Risk: Consistent investing reduces the risk of making wrong market timing decisions.

Cons of SIP

- No Control Over Market Timing: Investments occur regardless of market conditions, potentially leading to lower returns during prolonged market downturns.

- Fixed Commitment: Requires a consistent cash flow for regular contributions.

- Limited Flexibility: Pre-determined schedule; cannot capitalize on sudden market opportunities.

- Long-Term Discipline Needed: To see significant growth, SIPs require long-term commitment and patience.

- Potential for Lower Returns: In a continuously rising market, lump sum investments may yield higher returns than SIPs.

2. Systematic Withdrawal Plan (SWP)

A Systematic Withdrawal Plan (SWP) allows investors to withdraw a fixed or variable amount from their mutual fund investment at regular intervals, such as monthly, quarterly, or annually. It provides a steady cash flow, making it ideal for retirees or those seeking a regular income stream without liquidating the entire investment.

Imagine you have been investing through SIPs for the past 20 years and have accumulated a substantial amount of wealth. Now, as you approach retirement or wish to leave your job to spend more time with your loved ones, an SWP can be a great option. It allows you to receive a steady monthly income while keeping the remaining investment intact, enabling the power of compounding to continue working on your remaining funds

How it Works:

- Investors choose the withdrawal amount and frequency.

- Mutual fund units are redeemed based on the Net Asset Value (NAV) on the withdrawal date.

- The remaining units continue to stay invested, allowing potential growth.

Features of Systematic Withdrawal Plan

- Regular Income: Provides a fixed stream of income at chosen intervals.

- Capital Appreciation: Unredeemed units remain invested, enabling potential capital growth.

- Customizable Withdrawals: Investors can choose the withdrawal amount and frequency.

- Tax Efficiency: In contrast, withdrawals are treated as capital gains, which can be more tax-efficient than interest income.

- Flexibility: Investors can start, stop, or modify SWP as per their financial needs.

- Hedge Against Market Volatility: Regular withdrawals reduce the impact of market fluctuations.

Pros of SWP

- Regular Income Stream: Ideal for retirees or those seeking a steady cash flow.

- Capital Gains Tax Benefit: In comparison, withdrawals are classified as capital gains, which may provide tax advantages over fixed deposits or bonds.

- Flexibility: Start, stop, or modify withdrawals according to changing financial needs.

- Wealth Preservation: Only a portion of units is redeemed, allowing the remaining investment to grow.

- Rupee Cost Averaging: By redeeming units at different NAVs, SWP helps in averaging the cost of withdrawal.

- No Lock-In Period: Unlike fixed deposits, SWPs offer liquidity without any lock-in period.

Cons of SWP

- Depletion of Principal: If the withdrawal amount exceeds the fund’s growth rate, consequently, the principal may get depleted over time.

- Market Risk: In a falling market, more units need to be redeemed, which may impact long-term wealth accumulation.

- No Guarantee of Returns: Returns depend on the fund’s performance, unlike fixed-income instruments like FDs or bonds.

- Capital Gains Tax: Withdrawals are subject to capital gains tax, which varies based on the holding period and type of mutual fund.

- Impact on Compounding: Regular withdrawals may reduce the compounding effect of the investment.

- Exit Load and Fees: Some mutual funds may charge an exit load or fees on premature withdrawals.

3. Systematic Transfer Plan (STP)

A Systematic Transfer Plan (STP) is an investment strategy that allows investors to transfer a fixed amount or units from one mutual fund scheme to another within the same fund house at regular intervals. It helps in balancing risk and reward by moving investments from one asset class to another, such as from equity to debt or vice versa.

How it Works:

- Investors choose the amount and frequency of the transfer (e.g., weekly, monthly, or quarterly).

- Units are redeemed from the source fund and invested in the target fund.

- This ensures systematic allocation without timing the market, helping in rebalancing the portfolio.

Features of Systematic Transfer Plan

- Systematic Transfer: Scheduled transfers from one fund to another.

- Flexibility in Frequency: Choose weekly, monthly, or quarterly transfers.

- Risk Management: Gradually shift investments to manage market volatility.

- No Market Timing Required: Reduces the need to time the market accurately.

- Capital Appreciation: The remaining balance continues to earn returns in the source fund.

- Tax Efficiency: Transfers are treated as redemptions and purchases, impacting capital gains tax.

Pros of STP

- Rupee Cost Averaging: Investments are made at different market levels, averaging the purchase cost and reducing market volatility impact.

- Disciplined Investment: Promotes regular and disciplined investing.

- Wealth Appreciation: Unredeemed units continue to grow in the source fund, maximizing returns.

- Risk Management: Gradual transfer reduces risk exposure, especially for investors nearing financial goals.

- Flexibility and Customization: Investors can choose the transfer amount, frequency, and duration as per their needs.

- Capital Preservation: Ideal for those wanting to lock in gains by shifting from equity to debt.

- No Lock-in Period: Investors have the flexibility to start, stop, or modify the STP as required.

Cons of STP

- Capital Gains Tax: Transfers are considered redemptions and are subject to capital gains tax.

- Exit Load: Some mutual funds charge an exit load if units are transferred within a specific period.

- Market Risk: Investments in the target fund are subject to market fluctuations.

- No Guaranteed Returns: Returns are based on the performance of the target fund.

- Higher Costs: Frequent transactions may lead to increased costs, including exit loads and capital gains tax.

- Requires Monitoring: Investors need to monitor and adjust the transfer strategy as per market trends.

4. Lumpsum Investment

A Lump Sum Investment in mutual funds involves investing a substantial amount of money in one go rather than spreading it out over time. This one-time investment strategy is suitable for investors with surplus funds who want to maximize returns by staying invested for the long term.

The primary risk of lump sum investments lies in the need to time the market accurately. If you invest during periods of high valuations, you may have to wait years for your investments to recover. You will be allotted units of mutual funds based on your time of investment.

How it Works:

- Investors invest a significant amount in a mutual fund scheme at once.

- Units are allotted based on the Net Asset Value (NAV) on the purchase date.

- The investment remains in the fund, benefiting from compounding and market appreciation over time.

Features of Lump Sum Investment

- One-Time Investment: A single, substantial investment in a mutual fund scheme.

- Long-Term Growth Potential: Ideal for long-term investors seeking capital appreciation.

- Compounding Returns: Earns returns on both principal and accumulated gains.

- Market Timing: Investment is exposed to market volatility based on entry timing.

- No Fixed Interval: Unlike SIPs, there are no periodic payments.

- Potential for High Returns: High-risk, high-reward investment approach.

Pros of Lump Sum Investment

- High Growth Potential: Investing a large amount at once can lead to significant wealth creation if the market performs well.

- Compounding Benefits: The entire investment grows together, maximizing the compounding effect.

- Convenience: One-time investment without the need to monitor or make periodic payments.

- Lower Average Cost: If invested during market lows, the cost per unit is lower, leading to higher potential gains.

- No Commitment to Recurring Payments: Unlike SIPs, there is no obligation for periodic payments, ensuring financial flexibility.

- Ideal for Long-Term Goals: Suitable for long-term goals like retirement, a child’s education, or buying a property.

Cons of Lump Sum Investment

- Market Timing Risk: Poor market timing can lead to significant losses if invested during a market high.

- High Volatility Exposure: The entire investment is exposed to market fluctuations, increasing risk.

- Psychological Pressure: High stakes can lead to stress and emotional decision-making.

- No Rupee Cost Averaging: Unlike SIPs, the investment doesn’t benefit from averaging out costs.

- Liquidity Constraints: Tied-up capital with limited access until redemption.

- Risk of Capital Erosion: In a bear market, the value of the entire investment may depreciate significantly.

5. Step – Up SIP

A Step-Up Systematic Investment Plan (SIP), also known as a Top-Up SIP, is a type of mutual fund investment strategy where the investor increases the SIP contribution periodically, usually annually. This method allows investors to gradually increase their investment amount in line with income growth, inflation, or changing financial goals.

How it Works:

- The investor sets up a SIP with an initial fixed amount.

- At a predefined interval (e.g., annually), the SIP amount is increased by a fixed percentage or a fixed amount.

- This gradual increase enhances the overall investment, leading to greater wealth accumulation over time.

Features of Step-Up SIP.

- Periodic Increment: SIP amount increases at regular intervals, usually annually.

- Flexible Increment Options: The increase can be by a

- Customizable: Investors can decide the frequency, amount, and duration of the increment.

- Power of Compounding: Increased contributions lead to higher compounding benefits over time.

- Goal-Oriented Investment: Helps in scaling investments to meet growing financial goals.

- Seamless Integration: Most mutual fund platforms and apps support Step-Up SIPs with easy modification.

Pros of Step-Up SIP

- Higher Wealth Accumulation: Gradual increase in SIP amount leads to substantial wealth creation.

- Inflation Hedge: By increasing contributions, the investment stays ahead of inflation.

- Aligns with Income Growth: Matches investment capacity with salary increments and bonuses.

- Power of Compounding: Boosts the compounding effect with higher contributions over time.

- Goal Achievement: It is easier to achieve long-term goals like retirement, child’s education, or buying a house.

- Disciplined Investing: Maintains a disciplined investment habit with built-in increments.

- Flexibility and Control: Investors have control over the increment amount and frequency.

Cons of Step-Up SIP

- Commitment to Higher Outflow: Requires a commitment to increase contributions, which may strain finances.

- Income Dependency: Not suitable for those with irregular income or job instability.

- Market Risk: Like all mutual fund investments, it is subject to market volatility and risks.

- Potential Liquidity Issues: Higher SIP amounts may impact liquidity and other financial obligations.

- Emotional Pressure: Some investors may feel pressured to continue higher contributions even during financial stress.

- Requires Planning: Needs careful planning to ensure that increments align with income growth.

Conclusion :

Different methods of investing in mutual funds, like SIP, Lump Sum, SWP, STP, and Step-Up SIP, offer unique ways to grow wealth and achieve financial goals. On one hand, SIP provides disciplined investing with rupee cost averaging, whereas Lump Sum offers capital appreciation when timed well. In contrast, SWP ensures a steady income stream, ideal for retirees, while STP strategically reallocates funds to balance risk and returns. Step-Up SIP lets you increase contributions over time, matching income growth. By choosing the method that aligns with your financial needs and goals, you can maximize returns and secure your financial future.

This guide provides a clear and insightful overview of mutual funds and their benefits. It’s helpful to understand how SIPs, SWPs, and STPs can optimize investments for long-term goals. The breakdown of mutual fund types based on asset class and risk profile is particularly useful for making informed decisions. The example of using SWPs for retirement planning is practical and easy to follow. How can one determine the best mutual fund category to align with their financial goals?

Hii adventure travel! Great question. To determine the best mutual fund category for your financial goals, assess your risk tolerance, investment horizon, and goal type (e.g., equity funds for growth, debt funds for stability, or hybrid funds for balance). Match these factors with the fund’s asset allocation and your risk appetite for optimal alignment with your defined financial goal.