If you want to achieve financial independence, the first step is understanding the difference between assets and liabilities. In Rich Dad, Poor Dad, Robert Kiyosaki breaks this down in a way that completely shifts how we think about money.

His big message? Financial success isn’t just about how much you earn—it’s about how you manage, invest, and grow your money. When you apply his insights, you can start making smarter financial decisions and building long-term wealth.

So, let’s know what Robert Kiyosaki defines about assets and liabilities and see how this simple shift in mindset can change the way you approach your finances!

Traditional Definitions vs. Robert Kiyosaki

In traditional accounting, assets are things you own that have value—like cash, real estate, stocks, or businesses. Liabilities, on the other hand, are debts or financial obligations you have to pay back over time. While this definition works great for businesses and financial reports, it doesn’t always help when it comes to growing personal wealth.

That’s where Robert Kiyosaki takes a different approach. He simplifies these definitions by focusing on cash flow, making it easier to understand how money actually moves in and out of your life:

- Assets put money into your pocket—like rental income, dividends from stocks, or profits from a business.

- Liabilities take money out of your pocket—things like mortgage payments, car loans, and credit card debt.

By looking at your finances this way, you can make smarter choices about what to buy, what to avoid, and how to grow your money over time. It’s all about building assets that work for you instead of piling up liabilities that drain your wallet! Sounds like a game-changer, right?

Rethinking Common Beliefs

Robert Kiyosaki challenges us to rethink how we see our financial choices. Here are a couple of everyday examples that show the difference between traditional thinking and a cash-flow-focused mindset:

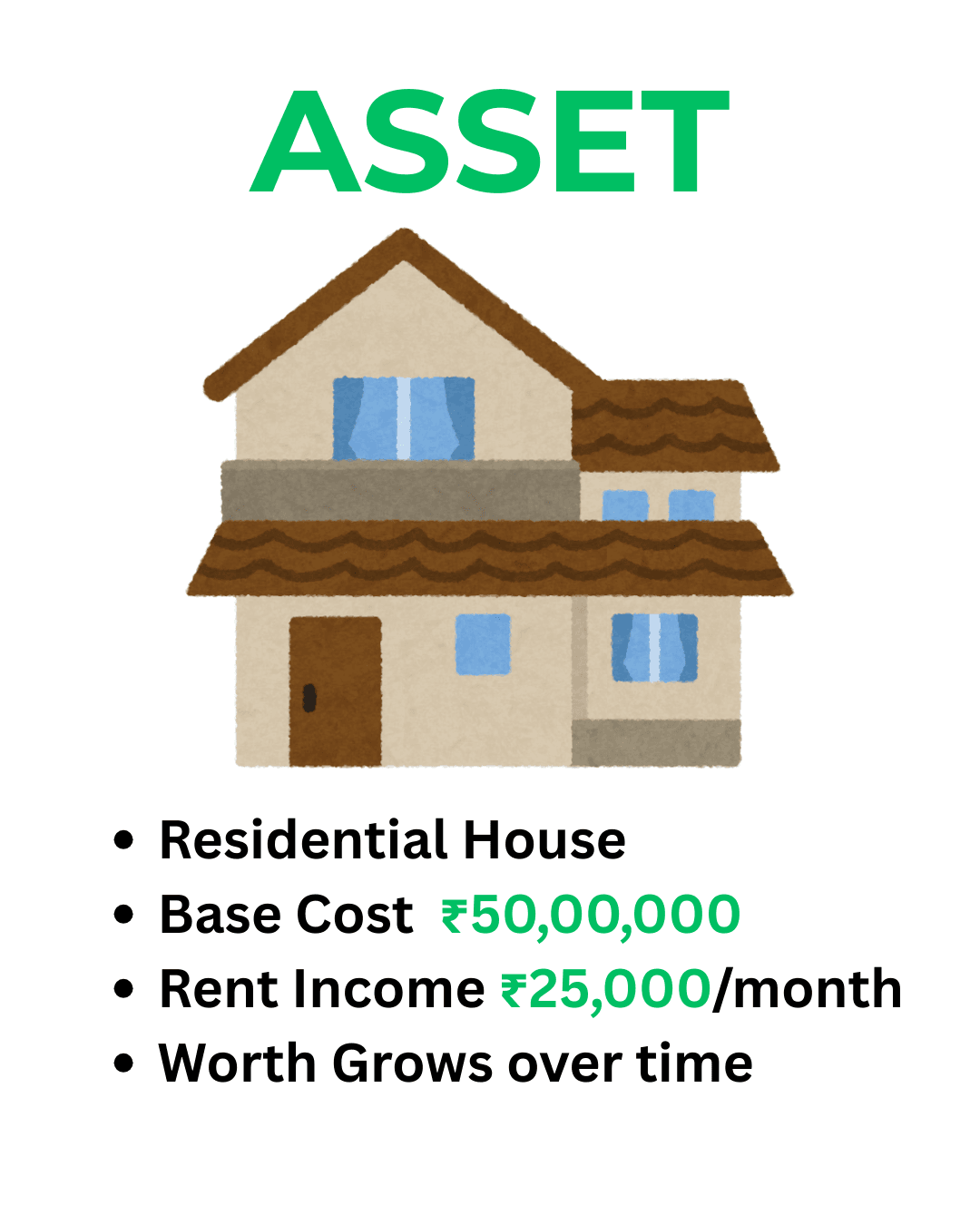

Your Home: Asset or Liability?

Most people believe their home is their biggest asset. But if your house isn’t making you money and instead costs you through mortgage payments, property taxes, maintenance, and insurance, it’s acting more like a liability. A home only becomes a true asset if it generates income—like renting out a portion of it or selling it later for a significant profit.

Your Car: More of a Money Pit than an Asset

A car might feel like an important purchase, but financially speaking, it’s usually a liability. Cars lose value over time and come with constant costs like gas, insurance, and repairs. Unless you’re using your car to make money—like driving for a ride-sharing service or business—it’s not really an asset.

This way of thinking helps us focus on building real wealth by acquiring true assets—things that put money in our pockets—instead of just collecting things that drain our finances. What’s one financial decision you’ve made that you now see in a new light?

To read the full book click on Rich Dad, Poor Dad

Building Wealth with Income-Generating Assets

If you want to grow your wealth and achieve financial independence, the goal is simple: build assets that put money in your pocket—even when you’re not actively working. These assets work for you, creating a steady stream of income. This way u can get the understanding of assets vs liabilities. Here are some great examples:

Ways to Make Your Money Work for You

- Rental Properties – If you own a property that brings in more rent than it costs to maintain, you’ve got a steady source of passive income and a property that may increase in value over time.

- Dividend-Paying Stocks – Some stocks pay regular dividends, meaning you get paid just for owning them. It’s like having a company send you a little paycheck every few months!

- Businesses – Running a business or investing in one, can generate income beyond a paycheck, giving you financial freedom and control over your earnings.

- Intellectual Property – Whether it’s writing a book, creating music, designing an app, or launching an online course, intellectual property can generate royalties or licensing fees long after the work is done.

Let’s say you buy a rental property that brings in Rs. 50,000 per month after expenses. Not only does the property grow in value over time, but that monthly income keeps rolling in. Now imagine you have multiple rental properties or dividend-paying stocks generating thousands in passive income. That’s how financial freedom starts!

The key takeaway? Focus on acquiring assets that work for you—so you’re not just trading time for money. What kind of asset would you be most interested in investing in?

Practical Steps to Shift Your Financial Mindset

Understanding the difference between assets and liabilities is a great start, but the real magic happens when you take action. If you want to transform your finances, here are some simple, practical steps to get started:

1. Take a Good Look at Your Finances

Make a list of everything you own and figure out if each item is an asset (puts money in your pocket) or a liability (takes money out). If something is draining your wallet without giving you financial returns, it’s time to rethink it.

2. Learn, Learn, Learn

Financial literacy is your best tool for making smart money moves. Read books and blogs, take courses, watch videos, or talk to experts to better understand how to spot and invest in income-generating assets. The more you know, the better decisions you’ll make!

3. Make Smarter Money Choices

Before making a big purchase, ask yourself: “Will this make me money or cost me money?” If it’s just an expense with no return, think twice or find a way to turn it into an asset.

4. Start Small, Then Build

You don’t need a ton of money to start investing. Begin with something manageable, like dividend stocks, peer-to-peer lending, or a small rental property. As you gain experience and grow your income, you can scale up to bigger investments.

5. Create Multiple Streams of Income

Relying on just one paycheck can be risky. The key to financial independence is having multiple income sources—whether it’s from rental properties, stocks, a side business, or digital products. The more you diversify, the more financial security you’ll have.

6. Cut Down on Liabilities & Unnecessary Expenses

Some liabilities are unavoidable, but you can reduce their impact. Paying off high-interest debt, avoiding unnecessary luxury purchases, and limiting depreciating assets (like fancy cars) will free up more money to invest in things that build wealth.

At the end of the day, financial freedom isn’t about how much you earn—it’s about how well you manage and grow your money by avoiding a few mistakes. To know the top 5 mistakes to avoid in your 20’s read our latest post on Mistakes to Avoid in your 20s

Final Thoughts

Robert Kiyosaki’s philosophy on assets vs liabilities provides a powerful and practical approach to personal finance. By focusing on acquiring income-generating assets and minimising liabilities, you can take control of your financial future.

The journey to financial independence doesn’t require winning the lottery or inheriting wealth—it starts with the right mindset and smart financial choices. By applying these principles consistently, you can create multiple income streams, achieve long-term financial security, and ultimately enjoy the freedom to live life on your own terms. What’s one step you can take today to start moving toward your financial goals? Comment below.